Press Room: Tax Release

Proposed Regulations on SALT Cap Workarounds Maintain Focus on State-Created Charities, But Remain Silent on Pass-Through Planning

Treasury and IRS released proposed rules incorporating earlier guidance on the treatment of payments made to charitable organizations in return for tax credits as payments of state or local taxes for federal income tax purposes. The issuance of proposed regulations follows the adoption of final regulations in June aimed at thwarting the use of state-created charitable funds as workarounds of the $10,000 cap on state and local tax (SALT) deductions.

Unaddressed by the proposed regulations are the SALT cap workarounds adopted by several states involving entity-level state income tax on pass-throughs, with offsetting state tax credits for the entity’s members.

Background

The Tax Cuts and Jobs Act (TCJA) capped at $10,000 the amount of state and local tax payments that filers could deduct from their federal tax returns. States such as California, Connecticut, New Jersey, New York, and Oregon responded by attempting to create workarounds designed to help residents circumvent the $10,000 limit on deductions for state and local taxes.

Under such plans, residents could, instead of paying state property tax, choose instead to donate to a state-created charitable fund. A resident could deduct the amount of the donation on their federal tax return and also receive a state tax credit. Both of these benefits would help mitigate the effect of the lower federal deduction for state and local taxes.

Although the Democratic-led House passed a bill to repeal the $10,000 cap, the measure is not likely to advance in the Republican-led Senate.

New Proposed Regulations

The proposed rules incorporate Notice 2019-12, related to the situation where the taxpayer’s state and local tax deduction is less than the $10,000 cap, offering a safe harbor where reduction of the charitable contribution deduction for the state and local tax credit is not necessary or is only partially necessary. The proposed rules also incorporate the safe harbor previously provided in Rev. Proc. 2019-12 for situations involving payments by business entities where a state and local tax credit is received in connection with a charitable contribution.

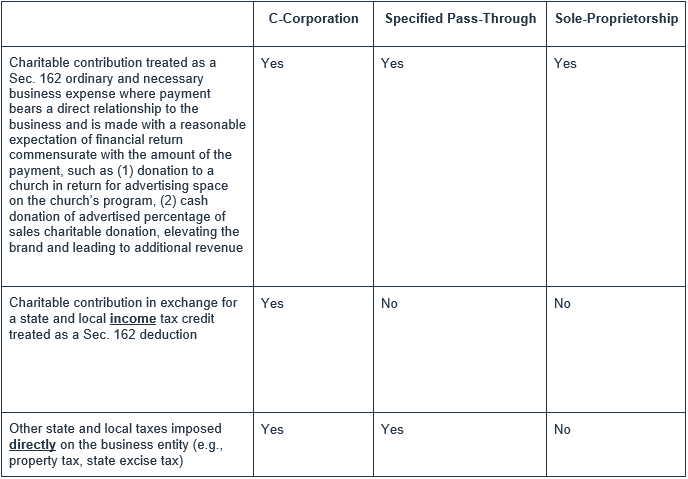

Under the safe harbor, a C corporation can generally treat a contribution for which it receives a credit as an ordinary and necessary business expense. A pass-through entity may treat a contribution as an ordinary and necessary business expense to the extent the tax credit reduces a state and local tax other than an income tax (such as a property tax) which is deducted by the entity and not passed through to the individual owners. A sole proprietorship cannot treat any contribution in exchange for a tax credit as an ordinary and necessary business expense.

For example, the proposed regulations explain that if a partnership donates $1,000 to a state-created charitable fund and it believes that doing so will generate a significant degree of name recognition and goodwill, the partnership may treat the payment as an expense of carrying on a trade or business. This result is unchanged if under the state’s tax credit program, the partnership is entitled to receive a $1,000 income tax credit as a result of the payment.

The proposed regulations also clarify that a payment to a charitable entity that results in a return benefit is a quid pro quo for purposes of the deduction for charitable contributions. As a result, the contribution is reduced by the amount of the return benefit for purposes of determining the amount allowable as a charitable contribution deduction.

Pass-Through Tax Not Addressed

Certain states have adopted new pass-through tax regimes that are aimed at working around the $10,000 cap. The taxes are imposed on the pass-through entity directly, and the pass-through entity member is provided a tax credit against individual level tax or an exclusion from income at the individual level. Connecticut and Wisconsin have such rules in place, Louisiana, Oklahoma, and Rhode Island have adopted new rules for 2019. One such measure passed the New Jersey Legislature and is awaiting the governor’s signature and other states are also considering changes. IRS and Treasury did not address these workarounds in the proposed regulations. It is unclear whether additional guidance will be issued to address these schemes, leaving taxpayers with uncertainty as to the availability of a federal tax deduction for state taxes paid implicated in these states. Taxpayers will need to carefully evaluate the viability of a federal tax deduction, taking into account the specific state workaround, whether it is voluntary, and whether the taxpayer could be viewed as receiving a quid pro quo which may negate the ability to tax a federal income tax deduction.

The Takeaway

The proposed rules further clarify that taxpayer may not circumvent the $10,000 SALT cap by making a donation to a state-created charity. Depending on the facts and circumstances, such expenditures could qualify as a deductible business expense, the proposed regulations state. Left unanswered by the proposal is the treatment of SALT cap workarounds involving entity-level state taxes on pass-through entities.

About the Authors

-

C. Ellen MacNeilWashington, D.C.

C. Ellen MacNeilWashington, D.C. -

Mary DuffyWashington, D.C.

Mary DuffyWashington, D.C.